Market Scenario

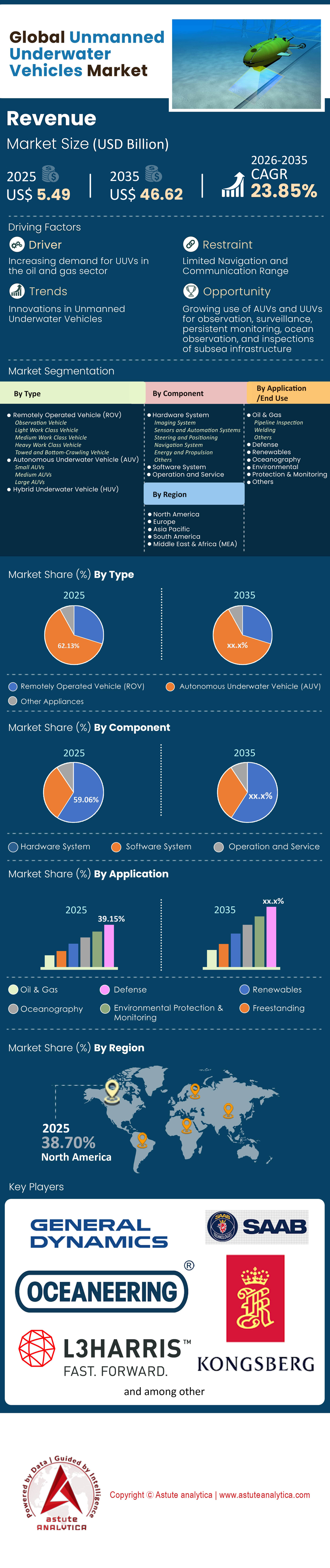

Unmanned underwater vehicles market was valued at US$ 5.49 billion in 2025 and is projected to hit the market valuation of US$ 46.62 billion by 2035 at a CAGR of 23.85% during the forecast period 2026–2035.

Key Findings

- Based on the type, Autonomous Underwater Vehicles (AUVs) commands a dominant market share of 62.13% in the market.

- By component, hardware systems is holding the highest share of 59.06%.

- By application, defense sector accounts for the largest share of 39.15%.

- North America, a longstanding frontrunner in the Unmanned underwater vehicles market, commands a substantial market share of over 38.70%.

As of 2025, the demand for unmanned underwater vehicles market has shifted from experimental curiosity to a strategic necessity, fundamentally altering the maritime landscape. In 2025, we are witnessing a "silent revolution" where the demand curve is no longer linear but exponential. This surge is primarily shaped by a dual-narrative: the urgent need for asymmetric naval defense and the commercial imperative to reduce the cost of managing offshore assets. Navies are moving away from relying solely on multi-billion-dollar manned submarines, pivoting instead toward "hybrid fleets" where autonomous systems handle the dull, dirty, and dangerous work. Consequently, the market is prioritizing endurance, autonomy, and payload flexibility over mere novelty.

Who Are the Key End Users and Where is the Demand Concentrated?

While the market is broadening, the Defense and Security sector remains the undisputed anchor tenant, accounting for the lion's share of procurement in the unmanned underwater vehicles market. The US Navy, for instance, allocated a specific USD 191.5 million in its FY2025 budget solely for the UUV "Family of Systems," signaling a massive commitment to integrating these assets into the fleet. Following closely are the Offshore Energy sectors—both oil and gas and the rapidly expanding offshore wind industry.

Geographically, the demand is highly concentrated within NATO member states and the Indo-Pacific region. The United States leads globally, driven by aggressive modernization programs. However, the United Kingdom and Australia are witnessing strong inflows of demand, heavily influenced by the AUKUS security pact. For example, Australia’s co-development of the Ghost Shark program, valued at AUD 140 million, highlights this regional intensity. In Europe, France and Norway are key hubs, with Norway’s Kongsberg maritime dominating the high-end survey market.

To Get more Insights, Request A Free Sample

What Major Application Areas Are Witnessing Strong Inflow of Demand?

Three specific applications in the unmanned underwater vehicles market are driving order books in 2025: Seabed Warfare (Critical Infrastructure Protection), Mine Countermeasures (MCM), and Ultra-Deepwater Inspection.

The sabotage of subsea cables and pipelines has terrified nations into action. Governments are now procuring Large Displacement UUVs (LDUUVs) specifically to patrol seabed infrastructure. This is evident in France’s procurement of Exail’s 6,000-meter rated AUVs in late 2024. Simultaneously, commercial operators are flooding the market with demand for inspection vehicles. Advanced Navigation’s Hydrus micro-AUV, priced around USD 55,000, has seen rapid adoption because it reduces survey costs by 75% compared to manned vessels. In the energy sector, vehicles like Kawasaki’s SPICE are now inspecting 20 kilometers of pipeline per dive at speeds of 4 knots, efficiency metrics that traditional ROVs simply cannot match.

How are Global Conflicts and Geopolitics Affecting the Market?

Geopolitical instability is the single greatest accelerator of the unmanned underwater vehicles market growth. The ongoing lessons from the Black Sea and tensions in the Red Sea have demonstrated that low-cost, expendable systems can deny sea control to larger naval powers. This has forced navies to rethink their "capital ship" strategies.

The concept of "attritable mass"—using cheap, swarm-capable drones that can be lost without major strategic impact—is driving procurement. For instance, the US Navy’s "Lionfish" program, with a contract ceiling of USD 347 million, allows for the procurement of up to 200 vehicles over five years. This volume-based approach is a direct response to the need for scalable assets in potential conflict zones. Furthermore, export controls are tightening; nations are using Foreign Military Sales (FMS) channels to arm allies, as seen with Japan’s 2025 order for over 12 Remus 300 units to bolster its island defenses.

Which Titans Dominate the Deep and Why?

The unmanned underwater vehicles market is dominated by a mix of established defense primes and agile disruptors. Huntington Ingalls Industries (HII) and Kongsberg Maritime sit at the top of the food chain. HII dominates because of its entrenched position with the US Navy and a diverse portfolio ranging from the portable Remus 300 to the long-endurance Remus 620. Kongsberg, conversely, rules the deep-water survey market. Their Hugin Endurance is unrivaled for commercial-defense crossover utility, boasting a 15-day autonomous endurance and a 1,200 nautical mile range.

However, Anduril Industries has emerged as a formidable disruptor in the unmanned underwater vehicles market. By applying a "software-first" approach and rapid manufacturing techniques, they are challenging the incumbents. Anduril’s new factory in Rhode Island, with a capacity to produce 200 Dive-LD units per year, addresses the industry's biggest bottleneck: production speed. Their Dive-LD, costing approximately USD 2.5 million, offers a cost-to-capability ratio that traditional aerospace firms struggle to match.

What Cutting-Edge Systems Hit the Water in 2024-2025?

Recent innovation in the unmanned underwater vehicles market has been defined by size and stamina. Boeing’s Orca XLUUV is perhaps the most impressive active platform. Measuring 26 meters and displacing 85 tons, this "unmanned submarine" delivered its second unit to the US Navy in early 2025. With a payload capacity of 8 tons and a staggering range of 6,500 nautical miles, it allows for mine-laying and surveillance missions in denied waters without risking a single sailor.

On the energy front, Cellula Robotics launched the Solus-XR, a hydrogen fuel-cell-powered vehicle that shattered endurance records. In sea trials, it demonstrated a range of 5,000 kilometers and a mission duration of 45 days, effectively bridging the gap between diesel-electric submarines and battery-powered AUVs. Similarly, the UK’s Project Cetus, a 17-tonne vehicle delivered in the 2024-2025 window, introduced a design capable of fitting into a standard shipping container, revolutionizing logistics for the Royal Navy.

What Are the Key Trends Shaping Future Market Growth?

As we move deeper into unmanned underwater vehicles market, three trends are sculpting the future of the industry:

- Data-as-a-Service (DaaS): Hardware sales are giving way to subscription models. Terradepth’s "Absolute Ocean" platform, launched in late 2024, exemplifies this. By delivering processed data within 24 hours—a massive improvement over previous weeks-long timelines—operators are paying for answers, not just robots. Early adopters have already reported a 20% revenue increase using this model.

- Swarming Capabilities: Single-unit missions are becoming obsolete for large-area denial in the unmanned underwater vehicles market. New software architectures allow heterogeneous swarms to communicate. RTsys recently demonstrated its Comet-300 operating in swarms of 10 vehicles, creating a synchronized sensor net that is exponentially harder for adversaries to detect or jam.

- Deep-Sea Resource Extraction: The push for critical minerals is driving vehicles deeper. Saab secured a USD 56.9 million (SEK 620 million) order for its Sabertooth vehicles, rated for 3,000 meters, specifically to support deep-sea mining and residency operations.

Segmental Analysis

By Type, Long-Range Autonomous Architectures Eliminate Surface Support and Extend Operational Reach

Autonomous Underwater Vehicles (AUVs) dominate the unmanned underwater vehicles market with a substantial 62.13% share because they fundamentally alter the economics of subsea operations by decoupling from expensive surface motherships. This "shore-to-shore" capability is a significant driver for commercial adoption, enabling vehicles to execute missions for extended periods without external intervention. Such operational independence dramatically reduces the daily costs associated with support vessels, making AUVs a far more cost-effective solution for a wide range of applications.

The unmanned underwater vehicles market is also seeing high-volume adoption of expeditionary-class AUVs. Deliveries of smaller UUVs to naval forces are scaling significantly, with these systems preferred over tethered remotely operated vehicles due to their ability to enable multi-agent "swarming" capabilities in critical areas like mine warfare and hydrography. The commercial energy sector further bolsters this segment, utilizing AUVs for resident subsea docking. This allows vehicles to remain submerged at offshore installations for months, drastically reducing human risk and the carbon footprint associated with surface operations.

By Component, Synthetic Aperture Sonars and Navigation Units Drive High-Value Hardware Expenditure

Hardware systems command a dominant market share of over 59.06% in the unmanned underwater vehicles market because the operational value of a UUV is entirely defined by the data density of its sensors and the precision of its navigation in GPS-denied environments. Synthetic Aperture Sonar (SAS) has emerged as a critical growth driver, rapidly replacing traditional side-scan sonar. These advanced sensors provide centimeter-resolution imagery at speeds that legacy systems cannot match. This high-resolution hardware is essential for detecting minute seabed threats or pipeline cracks, necessitating frequent, high-cost upgrades to maintain operational effectiveness.

Simultaneously, the demand for high-grade Inertial Navigation Systems (INS) is non-negotiable for achieving long-endurance autonomy across the unmanned underwater vehicles market. Without these advanced gyroscopic systems, an AUV would drift kilometers off-course during deep dives, rendering mission data useless. Furthermore, hardware dominance is sustained by the transition to pressure-tolerant Lithium-polymer batteries. These batteries eliminate the need for heavy, bulky pressure vessels, allowing for deeper operational ratings without increasing vehicle size. This evolution in subsystem technology forces operators to continually invest in hardware retrofits to maintain competitive range and endurance capabilities.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Application, Seabed Warfare Strategies and Mine Countermeasures Fuel Defense Sector Dominance

The defense sector leads the unmanned underwater vehicles market with over 39.15% market share due to an urgent strategic pivot from traditional Mine Countermeasures (MCM) to Seabed Warfare. This new doctrine focuses on the protection of critical underwater infrastructure, such as data cables and pipelines. This strategic shift is being formalized by international alliances, which are designing networks specifically to integrate UUVs for infrastructure surveillance. Consequently, navies are procuring large-displacement UUVs capable of persistent patrol, enabling them to monitor vast areas of the seabed.

In the MCM domain, the dominance in the unmanned underwater vehicles market is sustained by the imperative to remove sailors entirely from minefields. Naval forces continue to scale programs that utilize UUVs equipped with low-frequency broadband sonar to detect buried mines that surface ships often miss. This dual demand—protecting critical seabed infrastructure against potential sabotage while simultaneously automating dangerous mine-hunting tasks—ensures the defense sector remains the primary financier of high-end UUV innovation and procurement.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America Dominates with 38.70% Share Driven by US Navy Investments

North America’s commanding 38.70% market share of the global unmanned underwater vehicles market is not accidental, it is cemented by the US Navy's aggressive modernization strategy and an unparalleled industrial base. In FY2025, the US Navy allocated a specific USD 191.5 million solely for the UUV "Family of Systems," creating a direct pipeline for procurement. This financial commitment is supported by massive manufacturing scaling, notably Anduril’s Rhode Island facility which targets a production capacity of 200 units annually to meet surge demand. Furthermore, the delivery of the second 85-ton Orca XLUUV by Boeing in early 2025 signifies a mature capability to field large, strategic assets. With Huntington Ingalls Industries executing a contract ceiling of USD 347 million for the Lionfish program, the region effectively controls the high-end technology stack, leveraging these platforms for both domestic defense and Foreign Military Sales.

Asia Pacific Accelerates as Geopolitical Tensions Fuel Rapid Acquisition in Region

Asia Pacific region is the fastest-growing unmanned underwater vehicles market hub, driven by the urgency of the AUKUS security pact and regional island defense strategies. Australia is a primary engine of this growth, with its Ghost Shark program—valued at AUD 140 million—delivering 3 prototypes ahead of schedule in 2024 to counter asymmetric threats. Japan is simultaneously bolstering its maritime walls, finalizing an order for over 12 Remus 300 units in July 2025 to monitor its vast exclusive economic zones. Beyond defense, the commercial sector is robust; Japanese innovation is evident in Kawasaki’s SPICE vehicles, which are now capable of inspecting 20 kilometers of subsea pipeline in a single dive, addressing the region's critical need for energy security and infrastructure resilience.

Europe Prioritizes Seabed Warfare Capabilities and Critical Offshore Infrastructure Protection Markets

Europe’s unmanned underwater vehicles market strength lies in its dual focus on seabed warfare and deep-water commercial inspection, a direct response to recent infrastructure sabotage events. The United Kingdom is leading strategic innovation with the delivery of the 17-tonne Project Cetus XLUUV, a contract valued at £15.4 million, designed specifically to protect subsea cables. France has mirrored this vigilance, procuring Exail AUVs rated for 6,000 meters to ensure deep-sea dominance. Simultaneously, the commercial sector remains a global powerhouse; Norway’s Kongsberg Maritime successfully deployed the Hugin Endurance with a 15-day autonomous range in 2025. Furthermore, Sweden’s Saab secured a massive USD 56.9 million order for its Sabertooth vehicles, solidifying Europe's leadership in the resident subsea vehicle market.

Recent Developments in Unmanned Underwater Vehicles Market

- Saab LUUV concept for Sweden: Saab signed a SEK 60 million contract with Sweden’s FMV (Dec 30, 2025) to design, build and test a Large Uncrewed Undersea Vehicle (LUUV) as a multi‑mission seabed surveillance and sensor platform.

- Anduril Ghost Shark contract in Australia: Australia’s Department of Defence contracted Anduril in 2025 to deliver and further develop the Ghost Shark Extra Large Autonomous Undersea Vehicle, with AUD 1.7 billion earmarked over five years and “dozens” of systems for the Royal Australian Navy from 2026.

- Anduril Copperhead underwater drone launchIn April 2025, Anduril unveiled Copperhead, a new unmanned undersea vehicle that can be deployed from its larger Dive‑LD and Dive‑XL UUVs, configurable as Copperhead‑M with a warhead for torpedo‑like roles or with alternative payloads.

- Exail ultra‑deep A6K AUV: Exail introduced a new ultra‑deep Autonomous Underwater Vehicle capable of 6,000‑meter operations for deep‑sea mining survey, pipeline inspection and scientific missions, expanding commercial and defense reach into hadal depths in late 2025.

- ALSEAMAR deep‑sea glider program: ALSEAMAR was selected in November 2025 to develop a 3,500‑meter‑rated deep‑sea AUV/glider funded by France, targeting long‑endurance surveillance and environmental data collection in challenging deep‑ocean conditions.

Top Players in the Unmanned Underwater Vehicles Market

- Andrews Survey

- Atlas Elektronik GmbH

- BAE Systems Plc

- BaltRobotics Sp.z.o.o.

- Boston Engineering Corporation

- DOF Subsea AS

- Forum Energy Technologies

- Fugro Subsea Services Ltd

- General Dynamics Mission Systems, Inc.

- Helix Energy Solutions

- i-Tech (Subsea 7)

- Kongsberg Gruppen ASA

- L3Harris Technologies, Inc.

- Lockheed Martin Corporation

- Oceaneering International Inc.

- Saab AB

- TechnipFMC plc

- Other Prominent Players

Market Segmentation Overview:

By Type

- Remotely Operated Vehicle (ROV)

- Observation Vehicle

- Light Work Class Vehicle

- Medium Work Class Vehicle

- Heavy Work Class Vehicle

- Towed and Bottom-Crawling Vehicle

- Autonomous Underwater Vehicle (AUV)

- Small AUVs

- Medium AUVs

- Large AUVs

- Hybrid Underwater Vehicle (HUV)

By Component

- Hardware System

- Imaging System

- Sensors and Automation Systems

- Steering and Positioning

- Navigation System

- Energy and Propulsion

- Others

- Software System

- Operation and Service

By Application/End Use

- Oil & Gas

- Pipeline Inspection

- Welding

- Others

- Defense

- Renewables

- Oceanography

- Environmental Protection & Monitoring

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

FREQUENTLY ASKED QUESTIONS

The market is poised for exponential growth, projected to surge from USD 5.49 billion in 2023 to USD 46.62 billion by 2035. This expansion represents a robust CAGR of 23.85%, driven by the transition from experimental prototypes to essential strategic assets in both naval defense and offshore energy sectors.

Demand is driven by a dual-narrative: the naval necessity for asymmetric defense to counter larger fleets with attritable mass, and the commercial imperative to slash operational costs. Operators are prioritizing endurance and autonomy to replace expensive manned surface vessels with hybrid fleets that handle hazardous and repetitive subsea tasks.

Recent sabotage of subsea cables and pipelines has forced nations to prioritize Critical Infrastructure Protection. This has triggered a surge in orders for Large Displacement UUVs (LDUUVs) in the unmanned underwater vehicles market, such as Exail’s 6,000-meter rated AUVs and the UK’s Project Cetus, specifically designed to patrol and secure vulnerable seabed assets against hybrid threats.

Technological leaps in hydrogen fuel cells and pressure-tolerant batteries are effectively removing the leash from UUVs. For example, Cellula Robotics' Solus-XR recently demonstrated a 45-day mission duration and a 5,000 km range, allowing vehicles to bridge the operational gap between diesel-electric submarines and traditional battery-powered AUVs.

The market is shifting from selling hardware to selling answers. Platforms like Terradepth’s Absolute Ocean allow operators to purchase processed data delivered within 24 hours rather than investing in vehicle ownership. Early adopters of this subscription-based model have reported revenue increases of 20%, signaling a move toward high-margin service contracts.

North America unmanned underwater vehicles market leads with a 38.70% market share, anchored by the US Navy’s USD 191.5 million investment in UUV systems for FY2025. However, the Asia Pacific region is witnessing the fastest acceleration, driven by the AUKUS pact and Australia’s AUD 1.7 billion commitment to the Ghost Shark program to counter regional tensions.

Disruptors are winning market share in unmanned underwater vehicles m by solving production bottlenecks through software-first manufacturing. Anduril Industries, for instance, is challenging incumbents by opening facilities capable of producing 200 Dive-LD units annually, offering rapid scalability and a lower cost-to-capability ratio (approx. USD 2.5 million per unit) compared to traditional aerospace timelines.

The economic shift is drastic. Micro-AUVs like Advanced Navigation’s Hydrus serve as a prime example, capable of reducing survey costs by 75% compared to manned vessel operations. Furthermore, autonomous vehicles are vastly more efficient. For instance, Kawasaki’s SPICE AUV can inspect 20 km of pipeline per dive, far outpacing the speed and cost-efficiency of traditional tethered ROVs.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |